In this article

Among startups, few financial instruments have gained popularity as quickly—or sparked as much debate—as the SAFE note. Introduced by Y Combinator in 2013, the Simple Agreement for Future Equity (SAFE) has become the go-to structure for pre-seed and seed-stage startups looking to raise capital fast and with minimal legal friction.

But while SAFE notes are often considered founder-friendly, they’re not without trade-offs. In 2025, as investor scrutiny tightens and round structures evolve, it’s more important than ever for founders to understand how SAFEs work, when to use them, and how to avoid common pitfalls.

What Is a Simple Agreement for Future Equity (SAFE Note)?

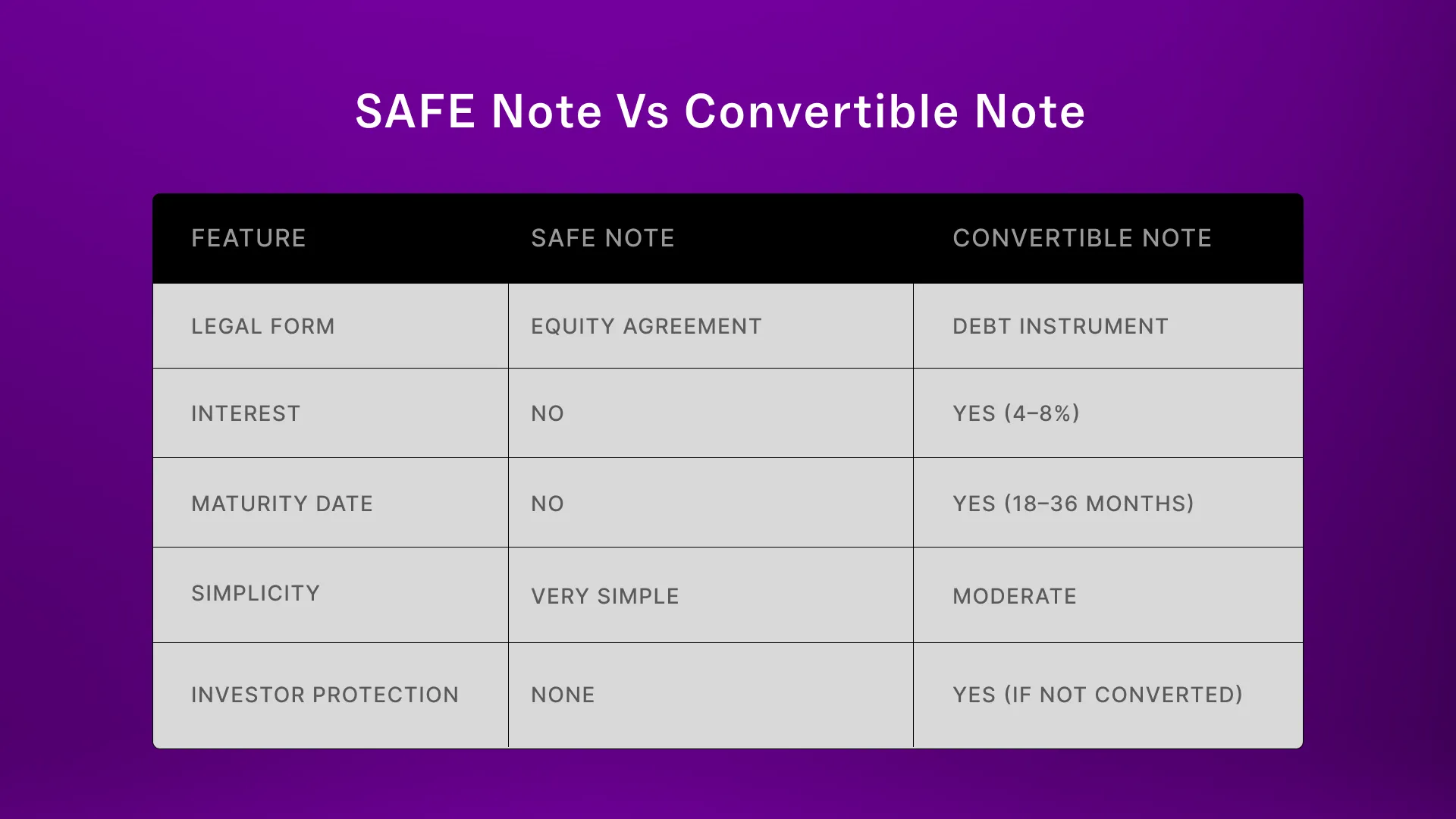

A Simple Agreement for Future Equity (SAFE) is a contractual agreement between a startup and its investors. It allows an investor to exchange capital for the right to receive equity in a future financing round—typically at a discount or valuation cap. Unlike a convertible note, a SAFE does not accrue interest or have a maturity date, making it a simpler and more founder-friendly structure.

SAFE was introduced by Y Combinator in late 2013 to help early-stage startups raise capital more easily. Since then, it has become one of the most widely used instruments in startup financing, particularly at the pre-seed and seed stages. Nearly all Y Combinator startups use SAFEs, and the format has since been adopted broadly across the venture ecosystem for its speed and efficiency.

Y Combinator has released four versions of the SAFE:

SAFE: Valuation cap, no discount

SAFE: Discount, no valuation cap

SAFE: Valuation cap and discount

SAFE: MFN, no valuation cap, no discount

While SAFEs are designed to be simple, founders and investors often amend terms with legal counsel to reflect their unique deal dynamics. Understanding the variations and implications of these different SAFE types is crucial to raising responsibly.

A SAFE note is a convertible security—not a loan—that gives an investor the right to receive equity in the company at a later date, usually during the next priced round. Unlike convertible notes, SAFEs:

Don’t accrue interest

Have no maturity date

Are not repayable debt

This simplicity makes SAFEs fast to execute, inexpensive to draft, and appealing to both founders and early believers who want to close quickly.

Key SAFE Note Terms

Valuation Cap – Sets the maximum valuation at which the SAFE converts.

Discount Rate – Gives investors a reduced price per share (typically 10–25%) in the next round.

MFN Clause (Most Favored Nation) – Lets investors benefit from better terms in future SAFEs.

Post-Money vs. Pre-Money SAFE – Post-money SAFEs (now standard) allow founders to calculate ownership dilution more accurately.

SAFE Note vs. Convertible Note

In 2025, SAFEs dominate early-stage funding. Carta data shows over 85% of pre-seed rounds now use SAFEs, especially among AI startups, where speed and momentum matter more than negotiation.

SAFEs are a good fit when:

You’re raising a small round quickly

You don’t want to set a valuation yet

You expect a priced round within 12–18 months

You want minimal legal and paperwork cost

But SAFEs are not ideal if:

You’re stacking multiple rounds without clarity

You want to give investors more downside protection

You’re raising from institutional VCs that prefer convertible notes or priced equity

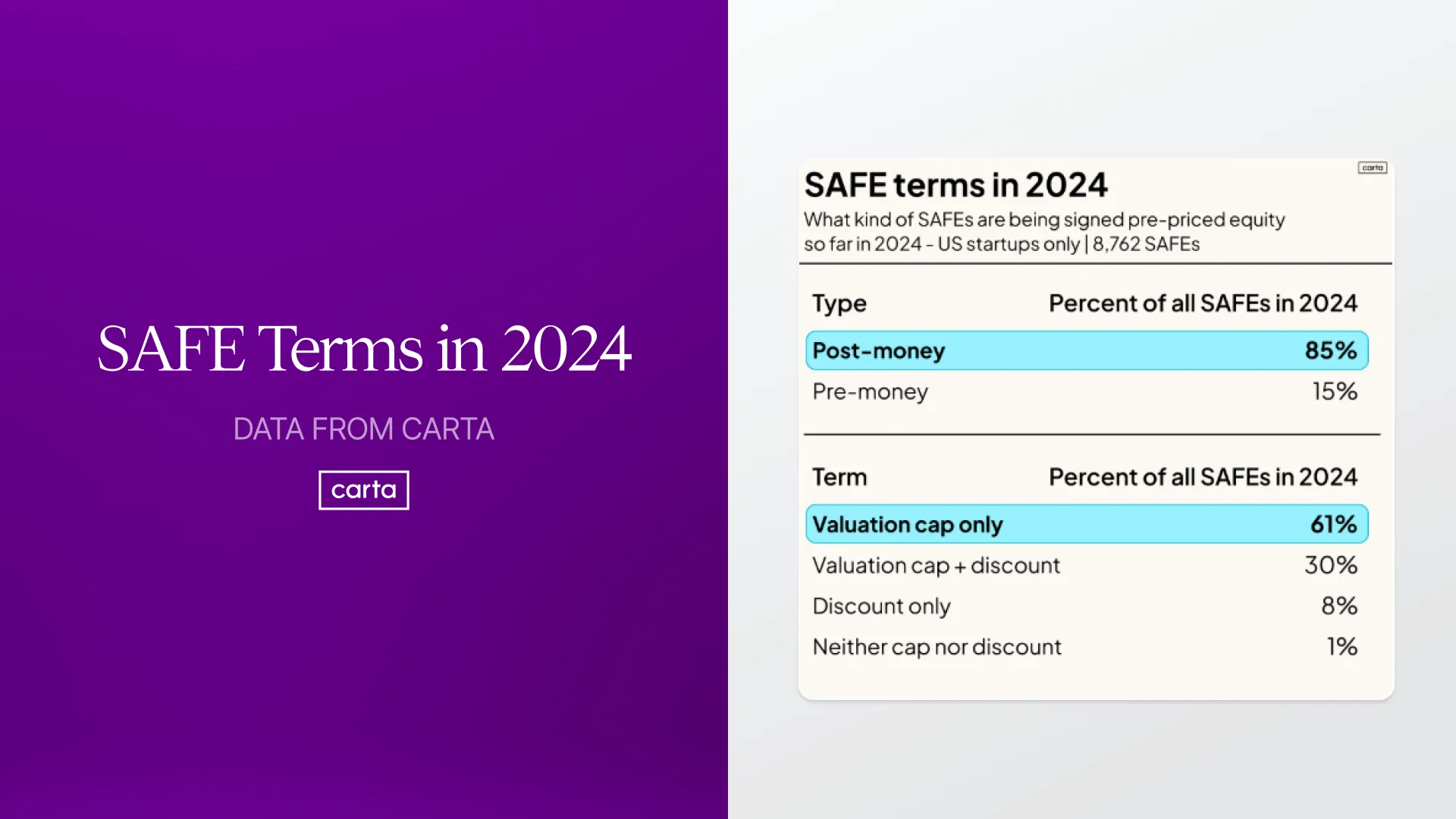

The Rise of Post-Money SAFEs

SAFE usage in 2024 has shown clear preferences in deal structure among early-stage U.S. startups. According to Carta, 85% of all SAFEs signed were post-money, now the default option due to its clarity around dilution. When it comes to terms, 61% of SAFEs used a valuation cap only, 30% included both a valuation cap and a discount, 8% used a discount only, and just 1% included neither—a signal that most investors still expect some form of compensation for early-stage risk.

Recent data from Carta shows that 61% of U.S. startup SAFEs in 2024 used only a valuation cap, 30% used a cap and a discount, 8% used just a discount, and 1% used neither. While the post-money SAFE was created to bring clarity to dilution, this data reveals a deeper shift—and some confusion—in how founders are structuring early-stage rounds.

Uncapped SAFEs, in particular, have drawn criticism. One investor remarked that the existence of SAFEs with neither cap nor discount suggests that "at least 1 in 12 VC funds has no idea what it’s doing." These instruments have become symbolic of overheated rounds and investor inexperience.

Y Combinator’s 2021 decision to remove the combination SAFE (with both a cap and discount) reflected their belief that either mechanism alone was sufficient. They argued that caps suit startups with relatively forecastable growth (like SaaS), while discounts apply to harder-to-value companies (e.g., biotech or hardware) still proving core feasibility. Combining both, they claimed, was often punitive and misaligned.

Yet, many founders and investors still favor the combo SAFE, despite YC’s stance. This has led to warped expectations: investors expect the standard 20% discount on top of a low cap, often creating excessive dilution and confusion when conversion happens.

Looking ahead, some argue that SAFE discounts should evolve—especially when used without caps. Larger discounts (potentially 50% or more) may better reflect investor risk in high-uncertainty ventures, while still avoiding premature valuation debates. This approach could revive SAFE utility in sectors like deep tech, where milestones take longer and capital needs are front-loaded.

Post-money SAFEs have become the industry standard. They calculate dilution based on the company’s cap table after the SAFE round, making it easier to see how much ownership founders are giving up.

While this clarity is helpful, it can lead to more dilution than founders expect—especially if multiple SAFEs are issued without planning.

Common Founder Mistakes With SAFEs

Not tracking total dilution from multiple SAFEs

Using uncapped SAFEs without leverage

Ignoring post-money modeling when raising

Failing to define a clear timeline for conversion

SAFE Notes and Today’s Market

The resurgence of SAFE notes in 2024 has been closely tied to the boom in AI startups and the fast-moving nature of early-stage fundraising. Business Insider reports that AI founders are using SAFEs to raise millions in days, valuing speed, simplicity, and control. With rising legal fees and intense competition for investor attention, founders often favor SAFEs over priced rounds to avoid immediate dilution and lengthy negotiations.

"Generally, SAFE notes are founder friendly," said Shaun Johnson, founding partner at AIX Ventures. "There’s no price being set, no board created, and control remains with the founders."

In sectors like AI—where capital intensity is high due to compute and talent costs—SAFEs are often the only practical way to raise large amounts quickly. Artisan AI, a Y Combinator company, reportedly raised $7.3 million using a SAFE, citing the ability to send docs and receive funds the same day.

But while this approach benefits speed, it creates challenges for investors. "You don’t know your ownership," said David Sainteff, partner at Global Founders Capital. That lack of clarity, especially in uncapped SAFEs, can erode trust and investor confidence long term.

Internationally, similar SAFE mechanisms are evolving. In Europe, firms like SeedLegals have adapted the SAFE model (via SeedFAST) to fit local legal systems, allowing startups in France and the UK to benefit from similar structures. Even high-profile founders like Monzo’s co-founder are now using SAFEs to launch new AI ventures.

This global adoption underscores the SAFE’s relevance in 2024—but it also signals a growing need for smarter structuring, clearer communication, and disciplined use. As the most commonly used fundraising tool for early-stage startups in 2025, the Simple Agreement for Future Equity allows founders to raise capital without setting a valuation. However, like all instruments, SAFE notes come with risks—especially around dilution and long-term investor expectations.

As the startup ecosystem matures, the shortcomings of SAFEs are becoming more apparent—particularly in how they affect dilution and cap table clarity. Originally designed by Y Combinator to simplify early-stage fundraising, SAFEs were intended to be fair to both founders and investors. But in practice, especially with repeated rounds of uncapped or low-cap SAFEs, many founders are now experiencing greater-than-expected dilution at the time of conversion.

One major issue is the misconception that the valuation cap represents a future floor, or that discounts set the minimum premium for the next round. This often leads founders to overlook the actual ownership impact of multiple SAFEs, especially when these notes are stacked over time without thorough modeling.

When a priced equity round finally occurs—often Series A—it’s not uncommon for founders to be shocked by their reduced ownership. A founder who believed they held 78% of their company may find themselves owning just 35% after conversion. The dilution isn’t caused by the new investors—it’s the result of earlier SAFE agreements whose effects were never fully understood or modeled.

Worse, a waterfall of existing SAFEs can make it difficult for new investors to meet their ownership targets, potentially stalling or killing a round altogether. This can result in the need for painful recapitalizations or down rounds simply to move forward.

Proactive founders are encouraged to work with legal counsel early to create pro-forma cap tables that show the impact of converting SAFEs before signing them. Understanding post-money valuation—and how multiple SAFEs compound dilution—is essential to avoid self-inflicted wounds.

In short, SAFEs remain a useful tool, but should be handled with caution. They are not a no-strings-attached way to raise capital. As one investor noted, "While rocket ship startups can overcome the structural issues of rolling notes, there are many more SAFE issuers than there are rocket ships."

In a more conservative investment climate, SAFEs remain popular, but not risk-free. Business Insider recently reported that AI founders are using SAFEs to raise millions in days—but some investors are wary of unclear ownership terms and lack of protections.

In general:

Hot startups can raise SAFEs with minimal friction

Founders should model dilution impact carefully

Investors are increasingly asking for caps and defined triggers

SAFE vs. Equity vs. Revenue-Based Financing

SAFE = fastest, cheapest, simplest

Convertible Note = more structured, includes interest and maturity

Priced Round = best for signaling, governance, and serious capital

Revenue-Based Financing = great for recurring revenue startups who want to avoid dilution

SAFE notes—or Simple Agreements for Future Equity—can be incredibly useful tools for early-stage founders—especially those moving fast, iterating quickly, or raising from angel investors. But they’re not a blank check.

Plan your cap table. Track dilution. Communicate clearly with investors. And always raise with a roadmap for your next round in mind.

Among startups, few financial instruments have gained popularity as quickly—or sparked as much debate—as the SAFE note. Introduced by Y Combinator in 2013, the Simple Agreement for Future Equity (SAFE) has become the go-to structure for pre-seed and seed-stage startups looking to raise capital fast and with minimal legal friction.

But while SAFE notes are often considered founder-friendly, they’re not without trade-offs. In 2025, as investor scrutiny tightens and round structures evolve, it’s more important than ever for founders to understand how SAFEs work, when to use them, and how to avoid common pitfalls.

What Is a Simple Agreement for Future Equity (SAFE Note)?

A Simple Agreement for Future Equity (SAFE) is a contractual agreement between a startup and its investors. It allows an investor to exchange capital for the right to receive equity in a future financing round—typically at a discount or valuation cap. Unlike a convertible note, a SAFE does not accrue interest or have a maturity date, making it a simpler and more founder-friendly structure.

SAFE was introduced by Y Combinator in late 2013 to help early-stage startups raise capital more easily. Since then, it has become one of the most widely used instruments in startup financing, particularly at the pre-seed and seed stages. Nearly all Y Combinator startups use SAFEs, and the format has since been adopted broadly across the venture ecosystem for its speed and efficiency.

Y Combinator has released four versions of the SAFE:

SAFE: Valuation cap, no discount

SAFE: Discount, no valuation cap

SAFE: Valuation cap and discount

SAFE: MFN, no valuation cap, no discount

While SAFEs are designed to be simple, founders and investors often amend terms with legal counsel to reflect their unique deal dynamics. Understanding the variations and implications of these different SAFE types is crucial to raising responsibly.

A SAFE note is a convertible security—not a loan—that gives an investor the right to receive equity in the company at a later date, usually during the next priced round. Unlike convertible notes, SAFEs:

Don’t accrue interest

Have no maturity date

Are not repayable debt

This simplicity makes SAFEs fast to execute, inexpensive to draft, and appealing to both founders and early believers who want to close quickly.

Key SAFE Note Terms

Valuation Cap – Sets the maximum valuation at which the SAFE converts.

Discount Rate – Gives investors a reduced price per share (typically 10–25%) in the next round.

MFN Clause (Most Favored Nation) – Lets investors benefit from better terms in future SAFEs.

Post-Money vs. Pre-Money SAFE – Post-money SAFEs (now standard) allow founders to calculate ownership dilution more accurately.

SAFE Note vs. Convertible Note

In 2025, SAFEs dominate early-stage funding. Carta data shows over 85% of pre-seed rounds now use SAFEs, especially among AI startups, where speed and momentum matter more than negotiation.

SAFEs are a good fit when:

You’re raising a small round quickly

You don’t want to set a valuation yet

You expect a priced round within 12–18 months

You want minimal legal and paperwork cost

But SAFEs are not ideal if:

You’re stacking multiple rounds without clarity

You want to give investors more downside protection

You’re raising from institutional VCs that prefer convertible notes or priced equity

The Rise of Post-Money SAFEs

SAFE usage in 2024 has shown clear preferences in deal structure among early-stage U.S. startups. According to Carta, 85% of all SAFEs signed were post-money, now the default option due to its clarity around dilution. When it comes to terms, 61% of SAFEs used a valuation cap only, 30% included both a valuation cap and a discount, 8% used a discount only, and just 1% included neither—a signal that most investors still expect some form of compensation for early-stage risk.

Recent data from Carta shows that 61% of U.S. startup SAFEs in 2024 used only a valuation cap, 30% used a cap and a discount, 8% used just a discount, and 1% used neither. While the post-money SAFE was created to bring clarity to dilution, this data reveals a deeper shift—and some confusion—in how founders are structuring early-stage rounds.

Uncapped SAFEs, in particular, have drawn criticism. One investor remarked that the existence of SAFEs with neither cap nor discount suggests that "at least 1 in 12 VC funds has no idea what it’s doing." These instruments have become symbolic of overheated rounds and investor inexperience.

Y Combinator’s 2021 decision to remove the combination SAFE (with both a cap and discount) reflected their belief that either mechanism alone was sufficient. They argued that caps suit startups with relatively forecastable growth (like SaaS), while discounts apply to harder-to-value companies (e.g., biotech or hardware) still proving core feasibility. Combining both, they claimed, was often punitive and misaligned.

Yet, many founders and investors still favor the combo SAFE, despite YC’s stance. This has led to warped expectations: investors expect the standard 20% discount on top of a low cap, often creating excessive dilution and confusion when conversion happens.

Looking ahead, some argue that SAFE discounts should evolve—especially when used without caps. Larger discounts (potentially 50% or more) may better reflect investor risk in high-uncertainty ventures, while still avoiding premature valuation debates. This approach could revive SAFE utility in sectors like deep tech, where milestones take longer and capital needs are front-loaded.

Post-money SAFEs have become the industry standard. They calculate dilution based on the company’s cap table after the SAFE round, making it easier to see how much ownership founders are giving up.

While this clarity is helpful, it can lead to more dilution than founders expect—especially if multiple SAFEs are issued without planning.

Common Founder Mistakes With SAFEs

Not tracking total dilution from multiple SAFEs

Using uncapped SAFEs without leverage

Ignoring post-money modeling when raising

Failing to define a clear timeline for conversion

SAFE Notes and Today’s Market

The resurgence of SAFE notes in 2024 has been closely tied to the boom in AI startups and the fast-moving nature of early-stage fundraising. Business Insider reports that AI founders are using SAFEs to raise millions in days, valuing speed, simplicity, and control. With rising legal fees and intense competition for investor attention, founders often favor SAFEs over priced rounds to avoid immediate dilution and lengthy negotiations.

"Generally, SAFE notes are founder friendly," said Shaun Johnson, founding partner at AIX Ventures. "There’s no price being set, no board created, and control remains with the founders."

In sectors like AI—where capital intensity is high due to compute and talent costs—SAFEs are often the only practical way to raise large amounts quickly. Artisan AI, a Y Combinator company, reportedly raised $7.3 million using a SAFE, citing the ability to send docs and receive funds the same day.

But while this approach benefits speed, it creates challenges for investors. "You don’t know your ownership," said David Sainteff, partner at Global Founders Capital. That lack of clarity, especially in uncapped SAFEs, can erode trust and investor confidence long term.

Internationally, similar SAFE mechanisms are evolving. In Europe, firms like SeedLegals have adapted the SAFE model (via SeedFAST) to fit local legal systems, allowing startups in France and the UK to benefit from similar structures. Even high-profile founders like Monzo’s co-founder are now using SAFEs to launch new AI ventures.

This global adoption underscores the SAFE’s relevance in 2024—but it also signals a growing need for smarter structuring, clearer communication, and disciplined use. As the most commonly used fundraising tool for early-stage startups in 2025, the Simple Agreement for Future Equity allows founders to raise capital without setting a valuation. However, like all instruments, SAFE notes come with risks—especially around dilution and long-term investor expectations.

As the startup ecosystem matures, the shortcomings of SAFEs are becoming more apparent—particularly in how they affect dilution and cap table clarity. Originally designed by Y Combinator to simplify early-stage fundraising, SAFEs were intended to be fair to both founders and investors. But in practice, especially with repeated rounds of uncapped or low-cap SAFEs, many founders are now experiencing greater-than-expected dilution at the time of conversion.

One major issue is the misconception that the valuation cap represents a future floor, or that discounts set the minimum premium for the next round. This often leads founders to overlook the actual ownership impact of multiple SAFEs, especially when these notes are stacked over time without thorough modeling.

When a priced equity round finally occurs—often Series A—it’s not uncommon for founders to be shocked by their reduced ownership. A founder who believed they held 78% of their company may find themselves owning just 35% after conversion. The dilution isn’t caused by the new investors—it’s the result of earlier SAFE agreements whose effects were never fully understood or modeled.

Worse, a waterfall of existing SAFEs can make it difficult for new investors to meet their ownership targets, potentially stalling or killing a round altogether. This can result in the need for painful recapitalizations or down rounds simply to move forward.

Proactive founders are encouraged to work with legal counsel early to create pro-forma cap tables that show the impact of converting SAFEs before signing them. Understanding post-money valuation—and how multiple SAFEs compound dilution—is essential to avoid self-inflicted wounds.

In short, SAFEs remain a useful tool, but should be handled with caution. They are not a no-strings-attached way to raise capital. As one investor noted, "While rocket ship startups can overcome the structural issues of rolling notes, there are many more SAFE issuers than there are rocket ships."

In a more conservative investment climate, SAFEs remain popular, but not risk-free. Business Insider recently reported that AI founders are using SAFEs to raise millions in days—but some investors are wary of unclear ownership terms and lack of protections.

In general:

Hot startups can raise SAFEs with minimal friction

Founders should model dilution impact carefully

Investors are increasingly asking for caps and defined triggers

SAFE vs. Equity vs. Revenue-Based Financing

SAFE = fastest, cheapest, simplest

Convertible Note = more structured, includes interest and maturity

Priced Round = best for signaling, governance, and serious capital

Revenue-Based Financing = great for recurring revenue startups who want to avoid dilution

SAFE notes—or Simple Agreements for Future Equity—can be incredibly useful tools for early-stage founders—especially those moving fast, iterating quickly, or raising from angel investors. But they’re not a blank check.

Plan your cap table. Track dilution. Communicate clearly with investors. And always raise with a roadmap for your next round in mind.

Frequently asked questions

Are SAFE notes risky for founders?

They can be. While SAFE notes are easy to issue, stacking multiple SAFEs without modeling the impact can lead to unexpected dilution. Founders should track conversion terms, post-money caps, and pro forma ownership well in advance of a priced round.

What is the difference between a SAFE note and a convertible note?

A SAFE note (Simple Agreement for Future Equity) is not a loan—it doesn't carry interest or a maturity date. Convertible notes are debt instruments that convert to equity and often include interest and repayment timelines. SAFEs are simpler and more founder-friendly but require careful dilution planning.

When should a startup use a SAFE note instead of raising a priced round?

SAFE notes are ideal for early-stage startups raising quickly with minimal legal complexity. They're best used before setting a valuation, typically during pre-seed or seed rounds. However, startups planning larger raises or seeking institutional investors may benefit from doing a priced round instead.

In Germany, Gilion operates as a loan broker. The loans are granted by a third party bank.

In Germany, Gilion operates as a loan broker. The loans are granted by a third party bank.

In Germany, Gilion operates as a loan broker. The loans are granted by a third party bank.

In Germany, Gilion operates as a loan broker. The loans are granted by a third party bank.